Scope 2 emissions come from the energy your organisation buys and uses, like electricity or heating. Reporting them accurately is essential for meeting regulations like the EU’s Corporate Sustainability Reporting Directive (CSRD) and the UK’s SECR framework. The GHG Protocol Scope 2 Guidance requires companies to report emissions using two methods:

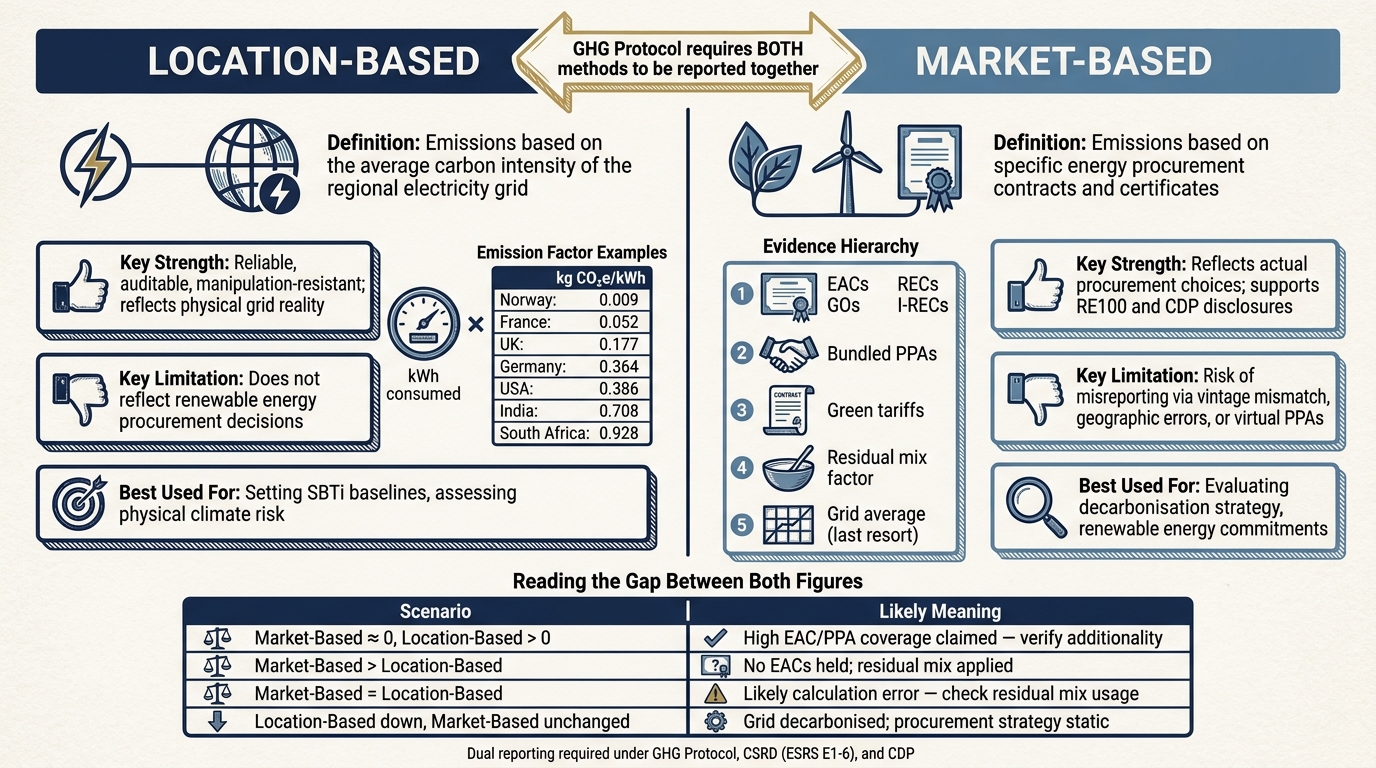

- Location-based: Calculates emissions based on the average carbon intensity of the electricity grid in the region where energy is consumed.

- Market-based: Focuses on emissions tied to specific energy procurement choices, such as renewable energy contracts or certificates.

Both methods must be reported together to ensure transparency and avoid cherry-picking favourable figures. Each method has strengths and limitations. Location-based reporting reflects physical grid emissions, while market-based reporting highlights energy procurement decisions. For organisations, especially private equity firms, understanding the difference helps evaluate risks and strategies effectively.

Key takeaway: Always report both figures and ensure accurate calculations using the correct emission factors and evidence for market-based claims.

Location-Based vs Market-Based Scope 2 Emissions: Key Differences at a Glance

Location-based Method: Calculating Emissions from the Grid

How Location-based Reporting Works

The location-based method determines Scope 2 emissions by applying the average carbon intensity of the local electricity grid to a facility's energy consumption. In simple terms, it multiplies the metered kilowatt-hour (kWh) usage by the emissions factor of the region, giving a clear picture of the grid's emissions, regardless of energy procurement choices.

The Greenhouse Gas (GHG) Protocol provides a hierarchy for selecting emission factors. Sub-national factors, like the US EPA eGRID subregions, take precedence when available. If these are not accessible, national sources such as DEFRA (UK), IEA, or ECCC are used, with supranational factors as the last option [2].

For companies regulated in the UK, DEFRA's conversion factors are compulsory for SECR compliance. Using IEA figures for UK operations is technically non-compliant [4]. These factors are updated annually, and the changes can be substantial. For instance, the UK's DEFRA grid factor dropped from 0.207 kg CO₂e/kWh in 2024 to 0.177 kg CO₂e/kWh in 2025. This 15% reduction reflects the closure of the country's last coal-fired power station [4][5]. Using outdated factors could inflate a company's Scope 2 emissions by about 17% if energy consumption remains constant [5].

Geographical differences play a huge role in this method. The carbon intensity of a single kWh varies greatly depending on where it is consumed:

| Country / Region | Factor (kg CO₂e/kWh) | Primary Source |

|---|---|---|

| Norway | 0.009 | IEA 2026 |

| France | 0.052 | IEA 2026 |

| United Kingdom | 0.177 | DEFRA 2025 |

| Germany | 0.364 | IEA 2026 |

| United States (National) | 0.386 | EPA eGRID 2024 |

| India | 0.708 | IEA 2026 |

| South Africa | 0.928 | IEA 2026 |

For portfolios spanning multiple countries, each asset's emissions must be calculated using its local factor. Relying on a blended average across the entire portfolio can introduce errors of over 20% [4].

Pros and Cons of Location-based Reporting

One of the main strengths of the location-based method is its reliability. The emissions data is sourced from publicly available and regularly audited figures, leaving little room for manipulation. This is why many organisations use it as a baseline for Science Based Targets (SBTi). The number only changes when the grid becomes cleaner, energy consumption decreases, or operations move to a different region [1].

"Location-based... optimises for physical-grid honesty: you cannot offset your way out of a coal grid." - Jeremiah Say, Lead Systems Architect, GreenCalculus [1]

However, this objectivity is also its biggest limitation. The location-based method does not account for energy procurement decisions. For example, a company that secures a long-term Power Purchase Agreement (PPA) with an offshore wind farm will report the same location-based emissions as a neighbouring company using standard grid electricity. This blind spot can be a challenge for private equity firms and others evaluating a company's decarbonisation efforts, as investments in renewable energy remain invisible in this metric [1][3].

sbb-itb-6ca8558

Market-based Method: Calculating Emissions from Procurement Contracts

How Market-based Reporting Works

The market-based method calculates emissions based on specific energy procurement contracts rather than relying on the grid's average carbon intensity, as the location-based method does. When these contracts involve renewable energy instruments, the emissions factor can drop to zero kg CO₂e/kWh for the covered consumption.

The GHG Protocol establishes a clear hierarchy for prioritising instruments in market-based reporting. At the top are Energy Attribute Certificates (EACs), which represent the environmental attributes of electricity generation. Different regions use distinct types of EACs: RECs in the US and Canada, Guarantees of Origin (GOs) in the EU (regulated by the AIB), REGOs (Renewable Energy Guarantees of Origin) in the UK post-Brexit, and I-RECs in regions like Asia, Africa, and South America that lack standardised national systems [1][6]. Below EACs in the hierarchy are bundled contracts, such as PPAs (Power Purchase Agreements), supplier-specific green tariffs, the residual mix factor, and finally, the grid-average factor, in descending order of preference [1].

A key concept here is the residual mix, which represents the grid's carbon intensity after accounting for claimed renewable generation. For example, in the UK, the 2025 DEFRA location-based factor is 0.177 kg CO₂e/kWh, but the residual mix for market-based reporting is closer to 0.200 kg CO₂e/kWh [1]. Companies that default to the grid average risk underestimating their emissions.

This structured framework helps provide a clearer picture of a company's energy procurement decisions, paving the way for evaluating the strengths and challenges of this method.

Strengths and Risks of Market-based Reporting

Market-based reporting adds depth to emissions accounting by focusing on actual procurement choices. Its primary strength lies in its ability to reflect these decisions accurately. For instance, a company with a long-term PPA tied to a new offshore wind farm can showcase its commitment through its market-based emissions figures - something the location-based method cannot highlight. This makes it a key tool for assessing decarbonisation strategies and is central to initiatives like RE100 and CDP's supply chain disclosures.

However, this method is not without its risks. Misreporting can occur if procurement instruments are mishandled or misunderstood. Common mistakes include:

- Vintage mismatch: EACs must be retired in the same reporting year as the consumption they cover.

- Geographic errors: For example, post-Brexit, UK consumption must be covered by REGOs, not GOs from EU countries like France.

- PPA limitations: Financial or 'virtual' PPAs that do not transfer EACs cannot be used to claim emissions reductions [1].

"The single most common Scope 2 audit finding is... companies reporting market-based equal to location-based without any EAC instruments held, on the assumption that 'no contract = use the grid factor.' The correct fallback is the residual mix factor." - Jeremiah Say, Lead Systems Architect, GreenCalculus [1]

Another area of debate is additionality - whether purchasing certificates genuinely contributes to new renewable energy capacity or merely shifts the attributes of existing generation. For example, unbundled EACs from older hydroelectric plants often face scrutiny under frameworks like CSRD and SBTi, which encourage companies to prioritise PPAs for new renewable projects as a more credible option [1].

Dual Reporting: Using Both Methods Together

What the Dual Reporting Requirement Means in Practice

The GHG Protocol doesn't ask companies to pick between location-based and market-based reporting - it requires both when contractual instruments are available [1]. This dual reporting rule is also part of CSRD (ESRS E1-6) and is a standard in CDP submissions. Providing only one figure, when both apply, is considered non-compliant.

The reason for this requirement is straightforward: it stops companies from showcasing only the more favourable figure while hiding the other. Every Scope 2 disclosure must include two separate totals: a location-based figure, calculated using the grid average (for instance, 0.177 kg CO₂e/kWh for the UK in 2025), and a market-based figure, which reflects actual procurement instruments or, if none are available, the residual mix factor [1].

This dual approach also offers private equity firms unique insights, as outlined below.

Reading Scope 2 Data in a Private Markets Context

Using these dual figures, private equity firms can distinguish between physical risks and procurement strategies. The location-based total highlights physical risks, while the market-based total reflects procurement choices.

The location-based total serves as a dependable measure for assessing physical risks. It shows the carbon intensity of the grid a portfolio company relies on, unaffected by administrative adjustments. It provides a consistent basis for comparing facilities across regions and for setting Science Based Targets (SBTi) [1].

The market-based total, on the other hand, reveals procurement behaviour. A market-based figure nearing zero, alongside a positive location-based figure, may indicate strong coverage through Energy Attribute Certificates (EACs) or Power Purchase Agreements (PPAs). However, these claims should be carefully reviewed, especially for additionality and certificate validity, before being accepted [1].

The gap between these two figures can act as a diagnostic tool. Here's a summary of common scenarios and their interpretations:

| Scenario | Likely Meaning | Suggested Action |

|---|---|---|

| MB ≈ 0, LB > 0 | High EAC or PPA coverage claimed | Verify additionality and check certificate vintage/geography |

| MB > LB | No EACs held; residual mix applied | Typical for firms without green strategies; confirm factor source |

| MB = LB | Likely a calculation error | Ensure residual mix, not grid average, was applied |

| LB down, MB unchanged | Grid decarbonised; procurement static | Likely reflects grid improvements, not company-led action |

When evaluating a portfolio company's Scope 2 disclosure, always verify the calculation method behind any key performance indicator. If only the market-based figure - particularly a near-zero one - is presented without the corresponding location-based total, it could signal a transparency issue worth addressing during due diligence [1].

Common Errors in Scope 2 Reporting and How to Avoid Them

Errors That Distort Scope 2 Calculations

Mistakes in Scope 2 reporting can sometimes go unnoticed, but they can significantly undermine the accuracy of your emissions data.

One common error involves using the national grid average instead of the residual mix factor when no contractual instruments are held. The residual mix excludes renewable energy already claimed by others, making it more accurate. It’s often 10–15% higher than the grid average, but many organisations overlook this distinction. As GreenCalculus notes:

"The single most common Scope 2 audit finding is... companies reporting market-based equal to location-based without any EAC instruments held, on the assumption that 'no contract = use the grid factor.'" - GreenCalculus [1]

Another frequent issue is mixing reporting methods in a single inventory. This blending creates figures that are neither physically nor contractually accurate, rendering them impossible to audit [1]. To comply, you must calculate market-based and location-based emissions as separate streams.

Additionally, ensure that Energy Attribute Certificates (EACs) meet specific criteria: they should be retired in the same reporting year, originate from the same market boundary, and align with the relevant certificate scheme. For instance, a French Guarantee of Origin cannot offset electricity use in the UK due to differences in certificate schemes [1][7]. Regularly updating emission factors from trusted sources is also crucial to avoid overstating emissions.

By addressing these errors, you can ensure your Scope 2 reporting withstands scrutiny.

Steps for Accurate Scope 2 Reporting

To improve accuracy, keep calculations for market-based and location-based reporting separate, as required by the GHG Protocol. This separation ensures compliance with dual reporting standards.

For market-based reporting, follow the GHG Protocol's evidence hierarchy. Begin with EACs, followed by bundled Power Purchase Agreements (PPAs), supplier-specific rates, the residual mix, and finally, the grid average (only if no residual mix is available) [1]. When using EACs, verify these three key points:

- The certificate was retired in the same reporting year as the energy consumption.

- It originates from the same market boundary (e.g., for UK electricity, use REGOs issued under the UK scheme).

- The environmental attributes have not been sold to another party [1][7].

To ensure compliance with standards and consistency across reporting periods, apply the following quality checks:

| Quality Check | What to Verify |

|---|---|

| Vintage | Certificate retired in the same year as consumption [1] |

| Geography | Certificate issued within the same market boundary (e.g., REGO for UK) [1] |

| Exclusivity | Attributes not double-counted or transferred to another party [7] |

| PPA Clauses | Contract explicitly transfers EACs to your organisation [1][7] |

Finally, remember to update emission factors annually using official sources like DESNZ or DEFRA. This keeps your figures accurate and aligned with the latest data.

Conclusion: Key Points for Private Equity Firms

Private equity firms can gain a lot from accurate Scope 2 reporting, as it provides insights into grid emissions and energy procurement strategies. Location-based figures show the carbon intensity of the grid a company is connected to, reflecting the physical reality of emissions. On the other hand, market-based figures assess how a company’s procurement strategy supports renewable energy through contracts, REGOs, or PPAs.

For private equity firms, location-based data offers a dependable foundation for setting decarbonisation baselines and evaluating physical climate risks across their portfolios. Meanwhile, market-based data reveals whether a company is actively contributing to decarbonisation through meaningful energy procurement or merely holding certificates that may not meet vintage or geographic standards [1][2].

Dual reporting is now a requirement under frameworks like the GHG Protocol, CSRD (ESRS E1-6), and CDP [1][2]. With the GHG Protocol planning stricter rules on hourly matching and unbundled certificate eligibility by 2027–2028, the bar for compliance will only rise [2]. Firms that incorporate rigorous dual-method reporting into their ESG due diligence today will be better prepared for these changes.

Additionally, the gap between location-based and market-based figures serves as a useful diagnostic tool. For example, a higher market-based figure often indicates that no renewable contracts are in place, while equal figures might point to a methodology error. Being able to clearly explain these gaps to auditors is where thorough Scope 2 reporting can become a real competitive edge during due diligence [1].