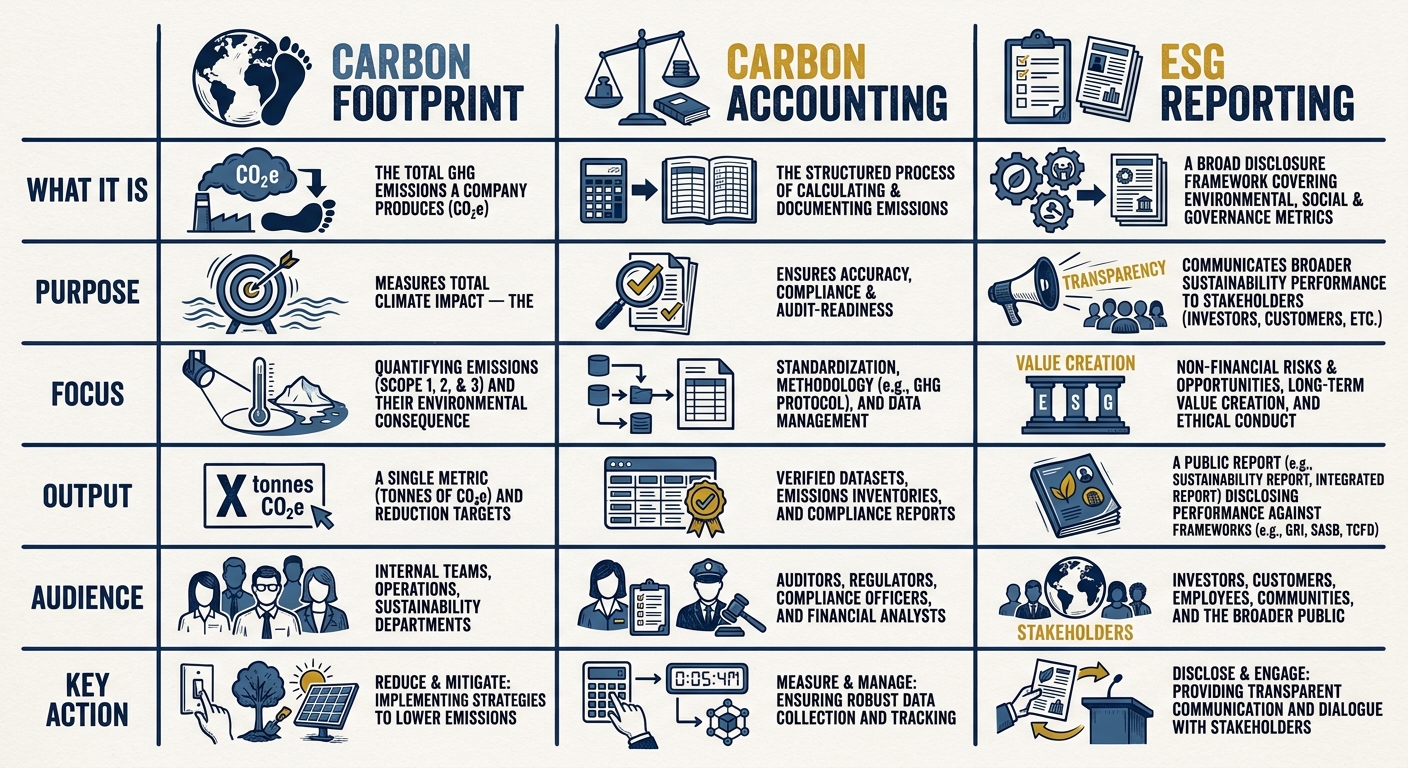

Carbon footprint, carbon accounting, and ESG reporting are related but distinct concepts often misunderstood in corporate settings. Here’s the quick breakdown:

- Carbon Footprint: The total greenhouse gas (GHG) emissions a company produces, measured in CO₂e. It’s the final number reflecting climate impact, covering Scope 1 (direct), Scope 2 (indirect from energy use), and Scope 3 (indirect across the supply chain).

- Carbon Accounting: The structured process of calculating and documenting emissions. It ensures data accuracy, auditability, and compliance with standards like the GHG Protocol.

- ESG Reporting: A broader framework that includes carbon data alongside social and governance metrics. It links emissions to a company’s strategy, risks, and financial health, often required under regulations like the EU’s Corporate Sustainability Reporting Directive (CSRD).

Key takeaway: Carbon footprint is the "result", carbon accounting is the "method", and ESG reporting is the "context" for disclosure and strategy.

Quick Comparison:

| Aspect | Carbon Footprint | Carbon Accounting | ESG Reporting |

|---|---|---|---|

| Purpose | Measures total emissions | Calculates and documents emissions | Discloses impact and financial risks |

| Scope | Total GHG emissions (CO₂e) | Scopes 1, 2, and 3 | Environmental, social, governance |

| Assurance | Often voluntary | Audit trails for accuracy | Mandatory third-party assurance |

| Regulation | Not always required | Supports compliance | Legally binding under CSRD, etc. |

Understanding these differences helps businesses meet regulatory demands, improve transparency, and manage climate-related risks effectively.

Carbon Footprint vs Carbon Accounting vs ESG Reporting: Key Differences

1. Carbon Footprint

A carbon footprint represents the total greenhouse gas emissions a company generates, expressed as carbon dioxide equivalent (CO₂e)[2]. It provides a single figure that encapsulates an organisation's impact on the climate at a specific point in time[2].

This calculation is broken down into three categories, or scopes:

- Scope 1: Direct emissions from a company’s owned or controlled operations.

- Scope 2: Indirect emissions from the energy a company purchases and uses.

- Scope 3: All other indirect emissions across the value chain, including suppliers, logistics, business travel, and the end-of-life of products.

Scope 3 often dominates a company’s footprint, accounting for 70–90% of emissions in most industries[4]. In financial services, this figure can rise to 98% or more[4].

"Scope 3... typically accounts for 70–90% of a company's total carbon footprint." - Paul Ferreira, Associate Climate Strategy Advisor, Normative [4]

In the realm of private markets due diligence, having an accurate carbon footprint is becoming a non-negotiable standard. By 2025, 640 investors managing assets worth US$127 trillion are expected to request environmental disclosures through CDP[1]. Such disclosures are critical because they provide insight into both an organisation's environmental impact and its exposure to climate-related financial risks. For example, emissions from corporate supply chains are, on average, 26 times greater than those from direct operations[1]. This highlights the inadequacy of focusing solely on Scopes 1 and 2.

The Science Based Targets initiative (SBTi) has set clear expectations: near-term goals (spanning 5–10 years) must address at least 67% of Scope 3 emissions, while long-term goals should cover 90%[4]. These benchmarks emphasise the need to comprehensively include all relevant emissions in a carbon footprint to ensure credible and effective transition strategies.

Accurately measuring this footprint is the first step, laying the foundation for the structured process of carbon accounting, which follows.

sbb-itb-6ca8558

2. Carbon Accounting

Carbon accounting is the structured process used to calculate an organisation's carbon footprint. It involves identifying, quantifying, and reporting greenhouse gas emissions to ensure accuracy and compliance with regulations. Here's a breakdown of the key steps involved:

First, organisations need to set their boundaries, defining which operations and activities will be included. Then, they identify emission sources across Scopes 1, 2, and 3. Next comes selecting a methodology, gathering relevant data, and applying verified emission factors. A vital part of this process is maintaining an audit log - a detailed, versioned record of the data sources, emission factors, and any exclusions. This ensures the inventory can pass third-party verification under standards like ISO 14064-3.

One common mistake is defining boundaries too narrowly. While a smaller footprint might look better on paper, it often means that key emission sources have been left out. To ensure credibility, it's essential to focus on the quality of data and the appropriateness of emission factors, not just the final numbers.

Carbon accounting isn’t a one-off task. It’s an ongoing process tied to base years and recalculation policies, ensuring consistency for year-on-year comparisons. This is particularly important in private markets, where due diligence demands robust and comparable data. With climate-related disclosures becoming a standard part of financial reporting - like the IFRS S2 Climate-related Disclosures, effective from 1 January 2024 [2] - investors now expect a solid, auditable foundation for assessing compliance and financial risks tied to climate change.

As Sofia Fominova, Co-Founder of Net0, explains:

"Carbon accounting is the data layer that determines whether an organisation can comply with mandatory climate disclosure regimes, retain access to capital, and stay in the supply chains of large customers." - Sofia Fominova, Net0 [1]

This meticulous approach ensures carbon accounting plays a central role in supporting broader ESG reporting needs.

3. ESG Reporting

ESG reporting takes carbon footprint and carbon accounting data a step further by embedding them into a broader framework that also includes governance and social metrics. Unlike carbon accounting, which focuses on quantifying emissions, ESG reporting evaluates what those emissions mean for a company’s strategy, stakeholders, and financial outlook. This makes ESG reporting a legally binding disclosure tool under frameworks like the EU’s Corporate Sustainability Reporting Directive (CSRD).

Here’s the key difference: carbon accounting asks, “How much did we emit?” while ESG reporting asks, “What does this mean for our business and its future?” Under the CSRD, companies must conduct a Double Materiality Assessment (DMA). This involves two perspectives: impact materiality (how the company’s actions affect the climate) and financial materiality (how climate change impacts the company’s financial health). The GHG inventory informs the first part, while scenario analysis addresses the second. Together, these elements position ESG reporting as a strategic tool that builds on established carbon metrics.

ESG reporting doesn’t just stop at presenting carbon data; it contextualises these numbers within a forward-looking strategy. For example, the CSRD requires companies to set decarbonisation milestones and assess the financial implications of both physical and transition risks over short, medium, and long-term periods. A crucial metric here is the GHG intensity ratio, expressed as tCO2e per €M net revenue, which ties emissions directly to financial performance [5].

"CSRD does not replace the calculation work - it wraps it in a legally binding disclosure structure." - Jeremiah Say, Lead Systems Architect, GreenCalculus [5]

This forward-looking approach is particularly critical for private markets, where due diligence processes will need to adapt to these regulatory changes. Starting in 2026, the Omnibus I Directive extends CSRD’s reach to EU companies with more than 1,000 employees and annual turnover exceeding €450 million. This adjustment reduces the scope to around 5,000 companies, compared to the initially estimated 50,000. Non-EU companies with significant operations in Europe are also included, making ESG reporting a pressing concern for portfolio companies with ties to the EU. Importantly, CSRD mandates limited third-party assurance for carbon data, meaning that the data must meet audit standards - it can’t just be directionally accurate. This underscores the need for precise carbon accounting and thorough footprint calculations.

Another compliance point to note: ESG frameworks like ESRS E1 require companies to report carbon credits and gross emissions separately to avoid greenwashing [5]. This is a common area where companies fall short during due diligence. For clarity on how to meet these requirements, frameworks such as CDP, EcoVadis, and CSRD offer detailed guidance and benchmarks.

Pros and Cons

Each of these three concepts plays a distinct role in assessing a company's climate credentials. To fully understand their importance, it's crucial to weigh their strengths and limitations. The table below highlights the key differences, offering a clearer picture of how these concepts fit into comprehensive due diligence.

| Feature | Carbon Footprint | Carbon Accounting | ESG Reporting (e.g., CSRD) |

|---|---|---|---|

| Primary Purpose | Communicates total emissions impact - the "number" [2] | Structured process for measuring and recording emissions - the "method" [2] | Regulatory transparency and double materiality disclosure [3] |

| Scope | Variable: product-level to portfolio-wide [2] | Scopes 1, 2, and 3; defined organisational boundaries [3] | Broad: includes operational control, absolute emissions, and intensity metrics [3] |

| Assurance | Often voluntary; high risk of data quality issues [6] | Focuses on auditability and evidence trails [6] | Mandatory limited assurance by independent third parties [5] |

| Metric | Absolute emissions (CO2e) [2] | Absolute emissions plus calculation methodologies [3] | Absolute gross emissions + GHG intensity (tCO2e per £M net revenue) [3] |

| Due Diligence Value | Provides a baseline for hotspot identification [2] | Verifies credibility and comparability of claims [2] | Reveals transition risks, financial exposure, and regulatory compliance [3] |

The carbon footprint is often the simplest metric to obtain, but it’s not always reliable on its own. Without a clear understanding of the accounting methodology behind it, there’s a risk of misrepresentation. For example, boundaries can be selectively drawn to exclude high-emission activities, making the data less trustworthy [2].

Carbon accounting steps in to bridge this gap. Its strength lies in its audit trail, offering documented evidence, consistent boundary definitions, and traceable emission factors. However, it’s not without challenges. Unlike financial accounting, carbon accounting lacks long-established standards. This can lead to inconsistencies, with reported emissions varying by as much as 25% to 45% for identical operations [6]. Moreover, only 38% of European companies reporting emissions can trace their Scope 3 data to primary sources, relying instead on industry averages [6].

"The gap between reported emissions and actual atmospheric impact has become a systemic risk to climate action itself." - European Commission [6]

ESG reporting provides the broadest perspective and carries significant regulatory weight. However, it comes with operational challenges. One major issue is the shortage of assurance professionals. Europe alone will need around 4,500 additional practitioners to meet demand between 2025 and 2028, but current training programmes are producing fewer than 1,500 annually [6]. For private investors, this is a critical point: an ESG report built on weak carbon accounting can be a major liability. Data quality matters - auditable emissions data has been linked to 23% better access to sustainability-linked financing, while poor data quality has been tied to stock price drops of 8% to 12% [6].

These considerations tie into frameworks like CDP, EcoVadis, and CSRD, all of which emphasise the importance of high-quality, auditable data. This analysis sets the stage for evaluating the due diligence frameworks discussed later.

Conclusion

The relationship between carbon footprint, carbon accounting, and ESG reporting is key to effective climate disclosure.

These three elements are interconnected: the carbon footprint represents the emissions inventory, carbon accounting is the process that creates it, and ESG reporting provides the structure for sharing it. Records of activities are transformed through carbon accounting into a footprint, which then feeds into disclosure frameworks. Whether a company is addressing a CDP questionnaire, an EcoVadis assessment, or filing under the CSRD's ESRS E1 standard, the accuracy of the carbon accounting methodology is critical to ensure the data withstands scrutiny.

This distinction is crucial because frameworks like CDP and CSRD require companies to detail how their numbers were calculated. By 2025, over 22,100 companies disclosed climate data through CDP, representing two-thirds of global market capitalisation [7]. Achieving this scale relies on consistent, auditable accounting processes. Using a single GHG Protocol-compliant inventory for both target-setting and mandatory disclosures helps avoid inconsistencies that could lead to audit failures [4]. Together, the footprint, accounting, and reporting frameworks form a seamless chain. For more guidance on compliance, consult the CDP, EcoVadis, and CSRD frameworks.